As China Slows and Tariffs Rise, Where Does the Middle East Turn?

Middle East countries are bracing for a dual economic shock. First, a slowing Chinese economy is weighing on global trade and demand, reducing China’s import appetite and curbing overseas investment flows. Second, the newly announced U.S. policy to impose a 10% universal tariff on all imports threatens to compound global trade uncertainty. These pressures are not yet fully felt, but their potential is clear. Together, they could prompt Gulf and broader Middle Eastern states to reassess economic exposure, reconfigure trade relationships, and accelerate plans for strategic diversification.

China’s Economies Woes Could Weigh Heavily on Gulf Exporters

The signs of China’s economic deceleration are mounting. China’s GDP grew by 4.9% in 2024, with forecasts suggesting a further slowdown to 4.5% in 2025. Retail sales growth remains below historical trendlines, while youth unemployment and property sector contraction continue to signal underlying weakness. Fixed asset investment grew modestly by 4.1% in early 2025, offering only a slight rebound from 2024 levels. While an uptick on paper, the figure reflects more a stabilization effort than a genuine recovery—driven largely by state-backed infrastructure projects rather than renewed private sector confidence. With deflation still a concern and the property sector lagging, this is still a sign of uncertainty, not resurgence

Middle Eastern states—particularly energy exporters—are watching closely. China remains a top destination for Gulf oil, petrochemicals, and industrial materials. A sustained slowdown could reduce demand, lower export volumes, and shrink budget margins. According to IMF estimates, a 1 percentage point rise in China’s growth can lift other countries by around 0.3 points. The inverse holds as well. China’s cooling economy—forecasted to grow at just 4.5% in 2025—could weigh heavily on Gulf states reliant on Chinese demand for energy and construction materials. For Middle Eastern countries, especially commodity exporters, this reinforces the need to reassess exposure and build more resilient, diversified trade portfolios

As economist Houze Song from MacroPolo points out, a weaker China has global ripple effects. Fewer imports mean less income for its trading partners. Investment slows. Infrastructure and energy projects stall. And that may leave Middle Eastern economies vulnerable.

Deflationary pressure is also mounting. Analysts now project China’s GDP deflator could fall to -0.2% in 2025—a sign that prices are dropping, consumer confidence is shaky, and firms may delay investments. This could push Beijing further inward, prioritizing domestic stability over outbound commitments. If China is focused on avoiding deflation and stabilizing consumption at home, it may cut back or slow foreign investments—including major Belt and Road projects and energy partnerships. For Middle East economies, this is another signal to reassess exposure to Chinese demand, and to prepare for a future where Beijing’s external economic footprint becomes more selective. That said, GCC countries are more likely to remain investment priorities, given their strategic value to China's energy security, digital expansion, and trade connectivity goals.

Selective Chinese Investment, and Strategic Openings for Gulf Capital

Chinese firms, who just a few years ago were ambitiously investing globally, are becoming more selective in their foreign dealings. Gulf partnerships continue in areas like smart cities, electric vehicles, and digital infrastructure, but broader Belt and Road investments have declined by 15% compared to 2019 levels.

This retrenchment has created a window of opportunity for Gulf sovereign wealth funds. With asset valuations down and credit conditions tightening in China, investors from the Gulf are moving into sectors that were once difficult to access—logistics, AI, semiconductors, and fintech (among others). In a notable reversal, Gulf capital is now flowing into China, rather than waiting on Chinese capital to flow outward.

This GCC pivot is strategic. Gulf countries are channeling capital into China’s domestic recovery across critical sectors, while simultaneously expanding their global investment footprint. In doing so, they hedge against economic volatility and strengthen their position as influential players in Asian markets. Crucially, they are no longer just recipients of foreign capital—they are emerging as capital-exporting powers, carving out a growing stake in China’s economy and buying greater leverage in the ever increasing interdependence.

Trump’s Tariffs Could Accelerate Trade Diversification

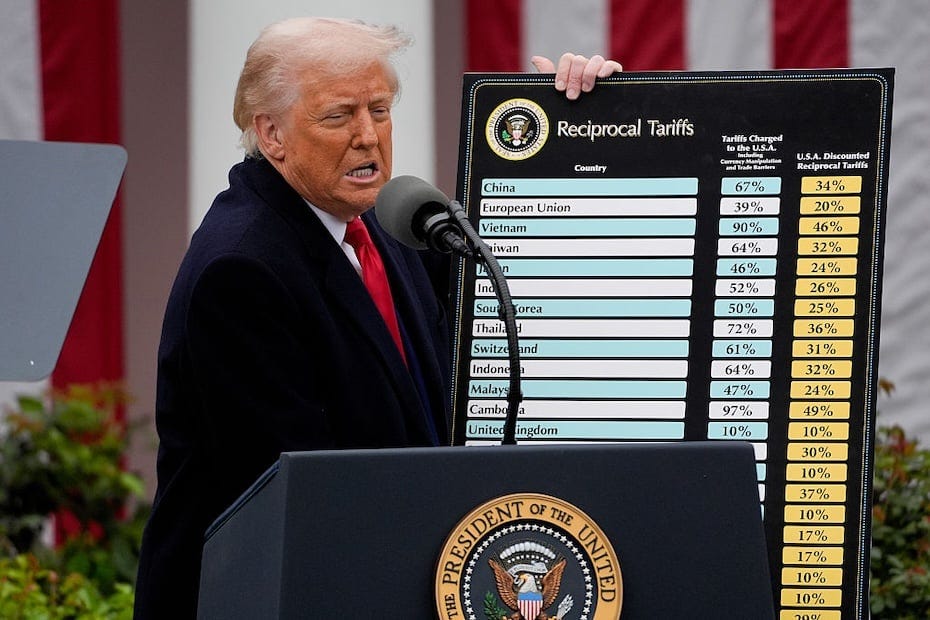

Meanwhile, U.S. trade policy is shifting—dramatically. On April 2, 2025, President Donald Trump announced a sweeping 10% universal tariff on all imports, set to take effect within days. The across-the-board levy is compounded by even steeper country-specific rates: Chinese exports to the U.S. now face a combined 54% tariff (if not higher), while goods from the EU and Japan are hit with new rates of 20% and 24%, respectively. In Beijing, several Chinese scholars I spoke with emphasized that China has prepared for the possibility of another trade war. They were clear-eyed about the economic impact, but adamant that President Xi is unlikely to yield to pressure from Washington. That message was echoed publicly by China’s Foreign Ministry spokesperson Lin Jian, who warned earlier this month: “The U.S. should return to the right track of dialogue and cooperation at an early date… if war is what the U.S. wants—be it a tariff war, a trade war, or any other type of war—we’re ready to fight till the end.”

The trade tariffs will also affect Middle Eastern economies, both directly and indirectly. While GCC states such as the UAE and Saudi Arabia may be able to weather the impact—due to fiscal buffers, trade flexibility, and diversified partners—others, like Jordan, will struggle under higher costs and more restricted market access.

Even where Middle Eastern exporters aren’t directly targeted, the spillover effects will be real. Rising trade frictions between the U.S., China, and Europe could increase transaction costs, disrupt shipping lanes, and trigger reciprocal tariffs that complicate Gulf access to critical export and re-export markets—especially for logistics hubs like Dubai and Jeddah.

In response, Middle Eastern states may begin to reassess the long-term reliability of U.S.-centric trade frameworks. The likely outcome? A broader recalibration—accelerating efforts to deepen commercial ties with Asia, Africa, and Europe, and reinforcing the push for greater strategic autonomy in navigating an increasingly multipolar global economy.

Trade Recalibration is a Strategic Imperative

This trade war may accelerate the drift toward a more fragmented global economy—and Gulf sovereign wealth funds are already rebalancing in anticipation. Over the past several years, GCC states began diversifying sources of goods and capital to reduce exposure to global shocks and better insulate themselves from major power trade disruptions. That trend is now intensifying. Investment flows are pivoting toward India, East Africa, and Southeast Asia, where supply chains are shifting and new growth hubs are emerging. Major ports like Jebel Ali, Duqm, and King Abdullah Port are being positioned as strategic nodes along intercontinental trade routes, including the India-Middle East-Europe Economic Corridor (IMEC).

At the same time, new free trade agreements—such as the UAE-India CEPA and a forthcoming GCC-UK deal—signal a broader appetite for diversification and risk mitigation. In this evolving landscape, the Gulf is increasingly serving as a hinge point in global supply chains: less dependent, more connected, and more resilient in the face of rising geopolitical and economic volatility.

As global power centers turn inward and trade tensions deepen, Middle Eastern states are not retreating—they’re repositioning.

Anticipating the Next Shift

China’s economic slowdown and U.S. trade nationalism will not reshape the Middle East economy overnight. But their combined weight may push regional governments and institutions to prepare for a broader economic diversification. GCC countries have anticipated the current economic shocks and have moved to mitigate their impact. It is testing partnerships, realigning capital, and strengthening its ability to weather disruption.

What emerges next may not be a realignment away from the U.S. or China—but rather a recalibration toward a more plural, self-directed economic order.

Bibliography

National Bureau of Statistics of China. “Statistical Communiqué of the People's Republic of China on the 2023 National Economic and Social Development.” National Bureau of Statistics of China, February 1, 2024. https://www.stats.gov.cn/english/PressRelease/202402/t20240201_1947119.html.

Reuters. “'Rotten Tail Kids': China’s Rising Youth Unemployment Breeds a New Working Class.” Reuters, August 21, 2024. https://www.reuters.com/world/china/rotten-tail-kids-chinas-rising-youth-unemployment-breeds-new-working-class-2024-08-21/.

China Banking News. “Chinese Property Still Accounts for a Quarter of GDP.” China Banking News. Accessed April 2, 2025.

Statista. “China: Outward Foreign Direct Investment (FDI) Flows 2010–2023.” Statista. Accessed April 2, 2025. https://www.statista.com/statistics/858019/china-outward-foreign-direct-investment-flows/.

Observatory of Economic Complexity (OEC). “China (CHN) and Oman (OMN) Trade.” OEC. Accessed April 2, 2025. https://oec.world/en/profile/bilateral-country/omn/partner/chn.

International Monetary Fund (IMF). “China’s Economy Is Rebounding but Reforms Are Still Needed.” IMF, February 2, 2023. https://www.imf.org/en/News/Articles/2023/02/02/cf-chinas-economy-is-rebounding-but-reforms-are-still-needed.

Green Finance & Development Center. “China Belt and Road Initiative (BRI) Investment Report 2023 H1.” FISF Fudan University, July 2023. https://greenfdc.org/china-belt-and-road-initiative-bri-investment-report-2023-h1/.

National Committee on U.S.-China Relations. “China’s Slowing Economy.” NCUSCR Podcast. Accessed April 2, 2025. https://www.ncuscr.org/podcast/chinas-slowing-economy.

U.S.-China Business Council. “China’s Economy Rallies to Reach Growth Target, 2025 Outlook Remains Uncertain.” USCBC, March 2025. https://www.uschina.org/articles/chinas-economy-rallies-to-reach-growth-target-2025-outlook-remains-uncertain/.

ING Think. “China’s First Data Dump of 2025 Beats Expectations.” ING Think, March 18, 2025. https://think.ing.com/articles/chinas-first-data-dump-of-2025-beats-expectations.

World Bank. “China.” World Bank. Accessed April 2, 2025. https://www.worldbank.org/en/country/china.

Reuters. “Trump to Escalate Global Trade Tensions with New Reciprocal Tariffs on U.S. Trading Partners.” Reuters, April 2, 2025. https://www.reuters.com/world/us/trump-escalate-global-trade-tensions-with-new-reciprocal-tariffs-us-trading-2025-04-02.

MarketWatch. “Trump’s ‘Liberation Day’ Tariffs to Come after Stock Markets Close as Taxes on Imports Stack Up.” MarketWatch, April 2, 2025. https://www.marketwatch.com/story/trumps-liberation-day-tariffs-to-come-after-stock-markets-close-as-taxes-on-imports-stack-up-fc0494ab.

Fractures in the global economic trade might be giving way to a new era of strategic realignment - the Saudi market is certainly becoming a favorite on global investors' watch

Just covered a bit of this here: https://saudiplus.substack.com/p/the-saudi-rhq-rush-global-companies > what do you think?